This report details some of the biggest trends and movements regarding M&A activity in the AEC industry as of the end of Q2 2023.

Zweig Group tracks every M&A transaction that takes place in the architecture, engineering, and construction (AEC) industry and reports on them on a weekly basis. This process allows us to stay up to date with the latest M&A trends in the AEC industry and report our findings to you. This report will detail some of the trends and movements regarding M&A activity in the AEC industry as of the end of Q2 2023.

As of June 30, 2023 there have been 311 closed transactions in the industry, an 8 percent increase over the 287 transactions that closed as of Q2 last year, while showing a decrease in transaction volume compared to the 173 closings in Q1 of 2023. As deal flow has sped up in Q2, we’ve seen architecture sellers represent a larger proportion of the total closings while environmental sellers have slipped into third place at 12 percent of total deal volume.

Of the 115 single discipline engineering firms that have been acquired so far this year, the majority of them (67 percent) were civil engineering firms, followed by MEP engineering (20 percent), and structural firms (13 percent). Of the 311 transactions that have taken place so far this year, 38 percent of sellers have completed projects in the commercial/retail sector. This is followed by public infrastructure at 26 percent, municipal government at 24 percent, higher education at 24 percent, and residential at 23 percent.

The large number of transactions in which the seller provided services in the commercial/retail are likely due to the abundance of firms that have capabilities within the sector relative to more regulated and specialized sectors such as public infrastructure and government. There are many firms that will provide services to primarily government clientele with sparse private projects, though the reverse is less common. From what we are seeing at Zweig Group, buyer demand is strongest in sectors that are directly benefiting from the Infrastructure Bill. These include water/wastewater, which is receiving $55 billion in new federal spending, roads and bridges ($111 billion), power/energy ($79 billion), and public transit ($39 billion). There are a slew of buyers who are looking to acquire to bolster their capabilities or expand into these sectors, but potential sellers that are operating in these sectors often have healthier financials, driving the purchase price up even before you take into consideration the increased buyer competition that comes with greater demand. This has made deal making more difficult for buyers looking to make plays in these sectors.

Of the 311 closings in the first half of the year, 210 took place in the United States, with transaction volume by state closely correlating to amount of funding that each state is receiving from the IIJA. These were also the most active states for buyers and sellers in FYE 2022 and Q1 of 2023.

So far in 2023, private equity groups have been a part of 37 percent of the deals that have been reported, showing a much larger proportion of the total than all of 2022 where PE groups represented 16 percent of total deal volume. For the sake of our data set, the buyer was considered to be private equity if it was the PE group itself or a private equity backed platform company. The median employee count of sellers through Q2 was 22 FTE, showing a decrease from last year’s median FTE size of 27.

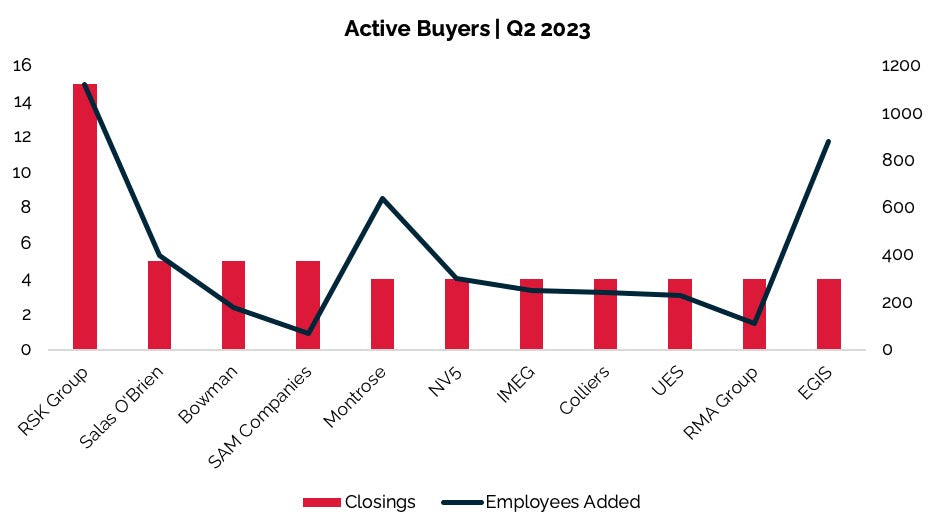

So far in 2023, the most acquisitive U.S. buyers by number of acquisitions are Salas O’brien, Bowman, and SAM Companies, each with five acquisitions completed in the first half of the year. There were quite a few U.S. firms that were close behind with four acquisitions in the first quarter, including Montrose, NV5, and IMEG, amongst others. The most acquisitive international buyer by number of acquisitions was RSK Group with 15 acquisitions throughout the U.K. and Denmark totaling roughly 1,100 new employees. RSK was followed by EGIS with four acquisitions around the globe totaling roughly 900 new employees, and Colliers with four acquisitions around the globe totaling roughly 240 employees.

In conclusion, the first half of the year has been highly active with 311 closed AEC transactions and a large uptick in the amount of buying activity from private equity firms compared to 2022. The states and markets that are experiencing the most buyer demand are those that are receiving the largest amount of financial support via the IIJA Bill, and the median FTE size of selling firms has decreased slightly to 22 FTE as smaller firms begin to adopt M&A as a growth strategy and platform companies fill in gaps with tuck in acquisitions.

Please reach out to achavez@zweiggroup.com with any questions.