Zweig Group believes that tracking and reporting on the financial standing of some of the industry’s leading, publicly traded firms will allow our readers to have another digestible form of information that will equip them with a greater understanding of the state of the industry. This monthly report, the Zweig Index, will examine 11 of the AEC industry’s leading firms on a monthly basis. This month we're focusing on Bowman.

Founded in 1995 and publicly traded as of May 2021, Bowman is a 1,600-person multi-disciplinary consultancy firm that offers real estate, energy, infrastructure, and environmental management solutions to public and private clients across the U.S. Bowman diversifies its revenue between building infrastructure (65 percent), transportation (17 percent), power and utilities (13 percent), and emerging markets (5 percent). Bowman (BWMN) was recently ranked 118 on the ENR Top 500 Design Firms list and is the 10th largest firm by market capitalization on the Zweig Index.

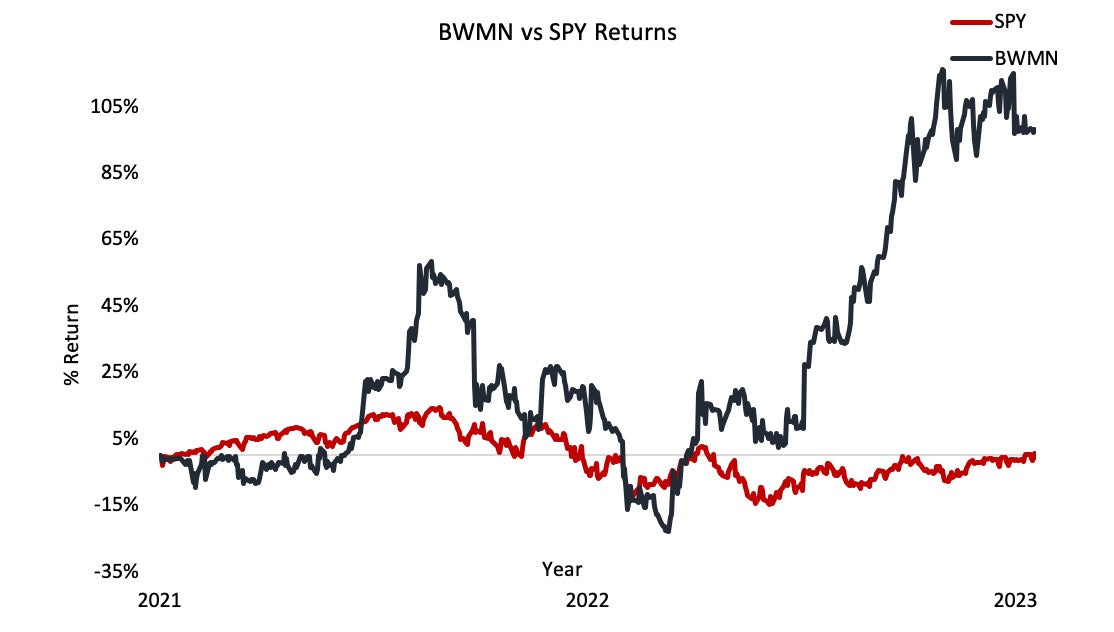

*Share price in USD as of 05/26/2023.

Financial highlights as of FYE 2022 ($USD):

- Gross revenue increased from $150 million to $262 million (+74.5 percent). The average 2022 gross revenue growth across all firms on the Zweig Index was 16.9 percent.

- Of the $111 million increase in gross revenue, acquisitions accounted for $66.5 million or 59.6 percent of total revenue.

- Net service revenue increased from $135 million to $235 million (+74.4 percent). The average 2022 NSR growth for firms on the Zweig Index was 19.9 percent.

- Adjusted EBITDA from continuing operations increased from $17 million to $34 million, which was 14.5 percent of NSR. The average adjusted EBITDA margin of firms on the Zweig Index has been 14.7 percent of net service revenue in 2022.

- In 2022, 79 percent of the firm’s total revenue was from private clients while the other 21 percent were public clients.

- Bowman’s operating segments are building infrastructure (65 percent), transportation (17 percent), power and utilities (13 percent), and emerging markets (5 percent).

The firm currently had $167 million worth of backlog entering 2023, which equates to 7.7 months of work for its current labor force.

Balance sheet ($USD):

- The firm’s cash and cash equivalents accounts decreased 35.6 percent, from $21 million to $13 million. Bowman’s current ratio is holding at 1.5x which is equivalent to the Zweig Index average for 2022.

- Quick ratio (cash + receivables / current liabilities) decreased from 1.8x to 1.1x. This decrease put Bowman’s quick ratio below the average of 1.2x for all firms.

- Debt to equity ratio increased from 0.16 in 2021 to 0.22 in 2022, a bit higher than the index average for 2022 which was 0.08.

Valuation metrics:

Enterprise value measures a company's total value, often used as a more comprehensive alternative to equity market capitalization. EV includes in its calculation the market capitalization of a company but also short-term and long-term debt and any cash or cash equivalents on the company's balance sheet. (Note that all estimated enterprise values are as of December 31.)

- Bowman’s EV increased from $233 million to $309 million. This increase was driven by the decrease in cash and cash equivalents as well as the rise in total debt.

- EV/NSR decreased from 1.7x to 1.3x.

- EV/adjusted EBITDA decreased from 14.1x to 9.1x.

- EV/Backlog increased from 1.4x to 1.8x.

Risks and opportunities:

Opportunities:

- Target Markets:

- High potential for reoccurring revenue and multi-year assignments.

- Increasing renewable energy, energy transition, and energy efficiency activities.

- Geographic and market diversity.

- Additional growth strategies:

- Acquisition: In-house acquisitions, diligence, and integrations teams to identify future acquisition targets.

- Geographic expansion: Targeting locations that have a million or larger population, complements or expands client opportunities, and leads to increasing availability of skilled labor force.

Risks:

- The loss of key personnel or inability to attract and retain qualified personnel could significantly disrupt business operations.

- Inability to compete effectively in a competitive market will lead to a decrease in market share and loss of business.

- Failure to integrate acquired businesses may cause multiple negative outcomes.

Acquisitions (2021-2022) ($USD)

Summary:

Bowman, one of the most acquisitive firms in the AEC industry with 16 acquisitions since 2021, had a very strong year growth-wise. The average 2022 total revenue growth across the Zweig Index was 16.9 percent, and Bowman saw revenue grow $112 million (+74.5 percent) largely due to acquisitions representing nearly 60 percent of gross revenue. Building infrastructure in 2022 increased $65 million, of which $37 million was attributed acquisitions. Bowman’s adjusted EBITDA as a percentage of NSR was comparable to the index average at 14.5 percent vs. 14.7 percent.

Bowman has only been a public company for two years but has shown growth year over year as they continue to expand revenue in all business segments. Likely in relation to their many acquisitions, Bowman’s debt to equity is one of the highest on the Zweig Index and has increased over 30 percent from the previous year, though their debt-to-income ratio remains strong at 10 percent. While Bowman highlights that they are bullish on all markets they serve, the company has just over half a years’ worth of backlog to help buffer against any economic setbacks, compared to the industry average of 15 months’ worth of backlog. The firm intends to continue to capitalize on the opportunity to acquire firms in our highly fragmented industry, and this will likely fuel continued revenue and EBITDA growth.