This article was originally published by Stambaugh Ness.

AEC firms may be leaving R&D tax credits untapped simply because they do not recognize the innovation already happening in their work.

Many architecture, engineering, and construction (AEC) firms leave significant money on the table every year simply because they assume research and development (R&D) tax credits are reserved only for tech or manufacturing companies. The reality? If your firm is solving complex design challenges, improving construction processes, or developing innovative systems, you may already qualify.

As scrutiny from the Internal Revenue Service continues to increase and reporting requirements become more detailed, understanding how to properly claim R&D tax credits for AEC firms is more important than ever.

So, what’s changed and how can your firm maximize the opportunity while staying compliant? Here’s what you need to know.

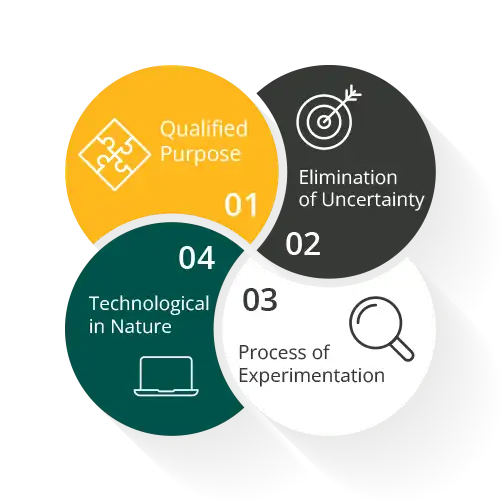

What qualifies as R&D for AEC firms?

Activities that involve technical uncertainty and a process of experimentation may qualify, including:

- Designing earthquake-resistant or structurally complex buildings

- Developing energy-efficient or net-zero systems

- Testing new materials or construction methods

- Improving project delivery processes or constructability

The IRS Four-Part Test serves as the foundation for every R&D tax credit claim.

One of the most common misconceptions is that “research” must happen in a lab. In AEC, it happens every day on job sites, in design software, and during problem-solving sessions.

Example: If your team evaluates multiple structural systems before finalizing a design, that iterative process, not just the final result, can qualify as R&D. For more details on qualifying activities, the IRS provides guidance here.

Why documentation matters more than ever

Today, claiming R&D tax credits for AEC firms requires more than just identifying qualifying work; it demands clear documentation.

What documentation does the IRS expect for R&D?

The IRS is looking for proof of process, not just your outcomes. That includes:

- Design iterations, sketches, and models

- Simulation results and testing data

- Meeting notes discussing technical challenges

- Time tracking is tied specifically to R&D activities

Example: Your team designs a new foundation system and tests multiple reinforcement approaches. If all you retain is a final drawing and generic time entries, your claim may not hold up under scrutiny.

Key takeaway: Think of documentation as your project’s “highlight reel.” The more clearly you can show how you solved a problem, the stronger your position. Utilizing a system that accurately tracks time and expenses and ties them to specific research activities can be a game-changer for tracking and documentation.

How contracts can make or break your eligibility

Many firms don’t realize that contract terms can directly impact their ability to claim the credit.

How do contracts affect R&D tax credit eligibility?

Two key factors matter:

- Financial risk: Did your firm bear the cost if the solution didn’t work?

- Rights to innovation: Can your firm reuse the knowledge or design?

Example: If you design a high-efficiency HVAC system but the client owns all rights and pays you regardless of success, the IRS may determine that you didn’t take on enough risk to qualify.

Key takeaway: Simple contract adjustments, such as retaining partial rights or tying compensation to outcomes, can preserve eligibility for R&D tax credits for AEC firms.

Connecting the dots: Nexus between work and expenses

Even when firms perform qualifying work, many claims fail due to weak connections between activities and costs.

What is Nexus and why is it important?

Nexus is the link between your R&D activities and the expenses you claim (wages, supplies, contractors, costs).

Example: Your engineers spend 200 hours developing a modular wall system, but your records only show “project work.” Without a clear tie to R&D, those hours may not qualify.

Key takeaway: Use project codes or tags in your time tracking system to link hours and expenses directly to R&D tasks. A clear bread-crumb trail makes it easier to defend your claim if it is reviewed.

Increased IRS reporting requirements

Recent updates to Form 6765 require more detailed information about research activities and business components. This means R&D tax credits for AEC firms are still valuable, but less forgiving when it comes to incomplete or vague filings.

Key takeaway: Build documentation and tracking into your workflow, not just at tax time. Staying organized makes responding to IRS questions much easier.

The bottom line: turning innovation into financial advantage

R&D tax credits remain one of the most powerful (and underutilized) incentives available to AEC firms. Success requires a proactive, structured approach.

Firms that maximize their credits consistently:

- Document as they go (not just at the end)

- Review contracts for risk and rights

- Connect expenses to specific R&D activities

- Stay on top of IRS reporting requirements

Treat your R&D claim like a well-designed project: with a strong foundation, clear plans, and no missing pieces. That way, your innovation earns the credit it deserves.

Take the next step

If your firm is innovating, and most AEC firms are, you likely have untapped opportunities for R&D tax credits. The challenge isn’t whether you qualify. It’s whether you’re capturing the full value of the work you’re already doing.

Working with an advisor who understands both tax regulations and the nuances of AEC projects can make the difference between a missed opportunity and a meaningful financial return.

Start the conversation today with Stambaugh Ness to evaluate your eligibility, strengthen your documentation, and ensure your innovation delivers the return it deserves.

|

Marla Miller, CPA, JD is managing director of Tax at Stambaugh Ness. Connect with her on LinkedIn. |